by Gary Rushin, CPA

Explore key techniques and applications of forensic accounting to enhance your financial investigations. Discover practical insights in our essential guide.

Introduction to Forensic Accounting

Forensic accounting involves using financial statement analysis and other techniques to investigate financial crimes and disputes. It requires a deep understanding of financial statements, accounting analysis, financial analysis, and financial reporting.

Forensic accountants use their skills to support law enforcement, government, and consulting agencies. They must have strong investigative skills and knowledge of financial processes to identify financial misconduct. Forensic accounting is critical in legal investigations where its findings are used as evidence in court proceedings.

In corporate fraud cases, including bankruptcy proceedings, divorce cases, insurance claims fraud, and business valuation disputes, forensic accounting can be applied.

Understanding Financial Statements

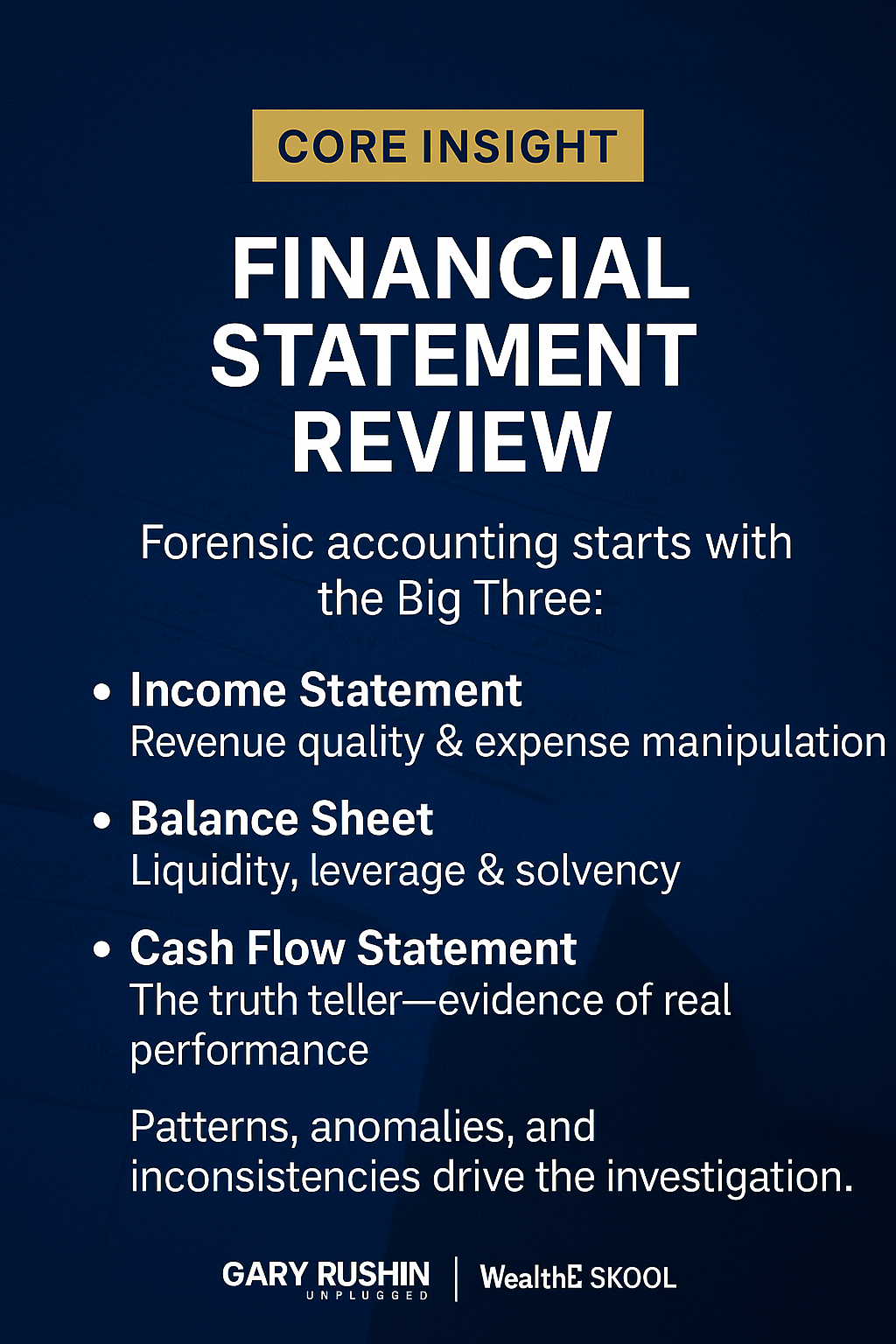

Financial statements, including the income statement, cash flow statement, and balance sheet, are crucial for financial analysis, as they provide insight into a company’s financial health and performance trends and support stakeholder decision-making. Reviewing a company’s financial statements is essential for understanding its financial position and health, as these documents provide detailed insights into stability, profitability, and risk.

Financial analysts use these statements to assess a company’s financial health and performance, gain insights into its performance, identify trends, and evaluate risk exposure by examining key performance metrics. The income statement shows revenue and expenses, while the cash flow statement shows cash inflows and outflows.

The balance sheet summarizes a company’s assets, liabilities, and shareholders’ equity at a specific point in time, providing a snapshot of the company’s financial position and is vital for guiding strategic decisions and future planning. When analyzing the balance sheet equation, it is essential to note that total assets must equal liabilities plus shareholders’ equity; total assets also serve as a base figure in vertical analysis to evaluate the relative weight of each item on the financial statement. Evaluating key financial ratios helps assess resource management and progress toward financial goals. The balance sheet provides a snapshot of a company’s financial position at a specific point in time.

Financial analysts rely on a company’s financial statements to assess its financial health and guide strategic decisions, ensuring a comprehensive understanding of its economic situation for effective planning and risk management.

Financial Statement Analysis

Financial statement analysis is a critical component of forensic accounting services. It involves reviewing a company’s financial statements to identify financial anomalies and potential fraud, and to assess the company’s financial health.

Financial analysts use horizontal analysis and vertical analysis to evaluate a company’s performance and identify trends. These techniques help assess a company’s performance by providing insights into its profitability, liquidity, and efficiency. Stakeholders, including investors and management, use financial analysis to make strategic decisions, and understanding a company’s performance and overall financial position is essential for effective decision-making. They also use financial ratios to assess a company’s profitability, efficiency, and leverage. Vertical analysis compares each line item on a financial statement as a percentage of a base figure within the same statement.

Performance evaluation is crucial in forensic accounting, as it helps stakeholders understand the company’s financial health and overall financial position.

Financial Analysis Techniques

Forensic accountants use various financial analysis techniques, including trend analysis and ratio analysis. These techniques help identify weaknesses in a company’s financial management and potential areas of financial fraud. Liquidity analysis tools include the quick ratio, which measures a company’s capacity to meet its short-term obligations using liquid assets and maintain financial stability.

Financial analysts also use accounting tools and software to analyze financial data and identify financial crimes. They must have a strong understanding of financial planning, risk management, and regulatory compliance. Account analysis involves a detailed examination of financial accounts to ensure accuracy, thereby improving budgeting, forecasting, and internal controls for businesses.

Forensic accountants also assess a company’s efficiency in utilizing resources, such as assets and accounts receivable, to generate revenue and maintain liquidity, focusing on key efficiency ratios to evaluate the company’s efficiency in operations and cash flow management. Periodic account analysis helps take corrective actions if required. Additionally, account analysis enhances transparency in financial management and can help in making informed strategic decisions.

These analyses help evaluate a company’s ability to meet its financial obligations, generate profits, and sustain operations.

Horizontal Analysis and Financial Reporting

Horizontal analysis involves comparing a company’s financial statements over time to identify trends and changes. This technique is useful for evaluating a company’s revenue growth by analyzing the company’s revenue figures over multiple periods, as well as assessing profitability and cash flows. Financial reporting is critical for providing stakeholders with accurate and timely information about a company’s financial performance.

Forensic accountants use horizontal analysis to identify financial anomalies and potential fraud. Horizontal analysis is another common method used in account analysis. Vertical analysis is also a common method used in account analysis.

Vertical analysis can highlight when costs are consuming too much of the company’s revenue relative to its historical performance. Regulatory filings, such as SEC filings, provide reliable data for conducting horizontal analysis and evaluating financial trends.

Cash Flow and Account Analysis

The cash flow statement shows a company’s ability to generate cash and pay its debts, as well as its capacity to meet various financial obligations and operational goals. Account analysis involves reviewing a company’s financial records to identify potential financial misconduct. Forensic accountants use cash flow analysis to evaluate a company’s ability to pay interest, dividends, and other expenses.

Ways to assess a company’s cash flow include free cash flow, which shows the amount of money left after paying for operating expenses and capital expenditures. Liquidity and coverage ratios are also used to evaluate a company’s ability to pay its short-term obligations; these ratios directly assess the company’s ability to pay and provide insight into overall financial stability.

Cash Flow and Account Analysis Involves

Financial analysts use account analysis to identify asset misappropriation, money laundering, and other financial crimes. The cash flow statement presents the changes in cash over a given period, along with the opening and closing cash balances.

Additionally, it provides data on the amount of cash or cash equivalents moving through the company via various inflows and outflows. Positive cash flow is essential to a business as it is used to pay dividends and expenses and fund expansions.

Operating cash flow is the cash generated by a business’s regular operating activities. The working capital ratio is a key performance indicator for assessing a company’s short-term financial health and operational efficiency. Cash flow can serve as a better indicator of a company’s financial health than profitability alone.

Balance Sheet and Financial Statement

The balance sheet is a foundational element of a company’s financial statements, offering a clear snapshot of its financial position at a specific point in time. By detailing assets, liabilities, and shareholders’ equity, the balance sheet provides valuable insights into a company’s overall financial health and stability.

Financial statement analysis of the balance sheet enables financial analysts to evaluate key financial ratios, such as the debt-to-equity ratio and the current ratio, which are essential for assessing a company’s leverage, liquidity, and solvency. These ratios help stakeholders understand how effectively a company manages its resources and obligations, and whether it is positioned for sustainable growth.

Analyzing the balance sheet also allows for the identification of trends and patterns in financial performance, which can signal strengths or highlight potential risks. When used in conjunction with the income statement and cash flow statement, the balance sheet becomes a powerful tool for gaining a comprehensive view of a company’s financial situation, supporting informed decision-making for investors, creditors, and management.

Income Statement and Financial Analysis

The income statement shows a company’s revenue and expenses over a specific period. Financial analysts use the income statement to evaluate a company’s profitability, efficiency, and revenue growth, with net income as the final figure that summarizes a company’s profitability after subtracting expenses from total revenue.

They also use the income statement to identify potential financial anomalies and areas of financial fraud. Forensic accountants use financial analysis techniques, such as trend and ratio analysis, to evaluate a company’s financial performance, including its ability to generate profits from operations and investments.

Key profitability ratios include gross profit margin, net profit margin, and return on equity. These ratios are used to assess a company’s profitability and compare it to industry standards. Profitability analysis involves measuring a company’s ability to generate profits using ratios like gross profit margin, net profit margin, and return on equity.

Key liquidity ratios include the current ratio and quick ratio. The income statement details a company’s revenues, expenses, gains, and losses, showing its profitability, with net income as the final figure summarizing the company’s.

Cash Flow Statement and Financial Reporting

The cash flow statement is a critical component of financial reporting, providing a transparent view of a company’s ability to generate and manage cash flows. This financial statement shows the movement of cash into and out of the business over a defined period, categorizing these flows into operating, investing, and financing activities.

By analyzing the cash flow statement, financial analysts can assess a company’s capacity to pay its debts, invest in growth opportunities, and return value to shareholders through dividends. The cash flow statement shows not only how much cash a company generates from its core operations, but also how it allocates cash for investments and finances its activities.

Through closely examining trends in cash flows, such as a consistent decline in operating cash flow or significant increases in capital expenditures, analysts can identify early warning signs of financial stress or opportunities for improved financial management.

Ultimately, the cash flow statement is indispensable for evaluating a company’s financial health and performance, enabling stakeholders to make strategic decisions based on a clear understanding of the company’s cash position and future prospects.

Legal & Regulatory Considerations in Forensic Accounting

Forensic accounting operates at the intersection of finance and law, making legal and regulatory considerations a cornerstone of effective forensic accounting services. Certified forensic accountants and certified fraud examiners must possess a thorough understanding of the legal environment in which they operate, as their work often supports litigation, regulatory investigations, and the prosecution of financial crimes such as financial fraud and money laundering.

A key responsibility for any forensic accountant is ensuring that all financial statement analysis and financial reporting adhere to the relevant legal and regulatory frameworks. This includes compliance with industry-specific regulations, anti-money laundering laws, and regulatory filing requirements. Accurate and transparent financial statements are essential not only for internal decision-making but also for meeting external legal obligations and supporting investigations into financial misconduct.

Forensic accountants must also be adept at gathering and analyzing financial data in a manner that meets legal standards for evidence. This involves maintaining meticulous documentation, ensuring the integrity of financial records, and establishing a clear chain of custody for all relevant data. These practices are critical when findings are presented in court or submitted to law enforcement agencies as part of a financial investigation.

In addition, forensic accounting services often require collaboration with government agencies, law enforcement, and regulatory bodies. Certified forensic accountants leverage their investigative skills to interpret complex financial statements, identify financial anomalies, and uncover evidence of financial crimes. Their expertise in financial statement analysis and financial reporting is vital for detecting irregularities that may indicate fraud or money laundering.

Ultimately, staying current with evolving legal requirements and regulatory standards is essential for forensic accountants. By integrating legal and regulatory considerations into every aspect of their work, forensic accounting professionals help ensure the integrity of financial processes, support the pursuit of justice, and protect organizations from the risks associated with financial crimes.

Draw Conclusions and Make Recommendations

Forensic accountants use their analysis to draw conclusions about a company’s financial health and performance. They also make recommendations to improve financial management, reduce risk, and prevent financial fraud. Based on their findings, forensic accountants may suggest adjustments to a company’s financial strategy to strengthen its future outlook and address identified weaknesses.

Certified forensic accountants and certified fraud examiners use their expertise to provide litigation support and consulting services. Forensic accountants trace the flow of funds, identify hidden assets, and uncover fraudulent schemes such as embezzlement. Forensic accountants help locate hidden assets in divorce or bankruptcy cases. They must have strong communication skills to present their findings and recommendations to stakeholders.

Forensic accountants prepare detailed reports and provide expert witness testimony in court. Additionally, they quantify damages in civil cases to determine economic loss in disputes. Forensic accountants maintain a clear chain of custody for all evidence to ensure its admissibility in court.

Best Practices for Forensic Accounting

Forensic accountants must follow best practices, including maintaining independence, objectivity, and confidentiality. They must also stay up to date with industry benchmarks, regulatory compliance, and new technologies. Forensic accounting services require a deep understanding of financial statements, financial analysis, and financial reporting. Forensic accountants must have strong investigative skills and a thorough understanding of financial processes to identify financial misconduct.

Common Challenges in Forensic Accounting

Forensic accountants face many challenges, including identifying financial anomalies, gathering relevant data, and staying up to date with new technologies. They must also navigate complex financial systems and identify potential areas of financial fraud.

Liquidity analysis assesses a company’s ability to pay off its short-term bills and debts using its most liquid assets. Forensic accounting services require strong communication skills and the ability to present complex financial information clearly and concisely.

Forensic accountants must be able to work with law enforcement, government, and consulting agencies to investigate financial crimes.

The Role of Technology in Forensic Accounting

Technology plays a critical role in forensic accounting, including providing tools for financial analysis, data visualization, and financial reporting. Forensic accountants use software and other technologies to analyze financial data, identify financial anomalies, and prevent financial fraud. They must stay up to date with new technologies and industry benchmarks to provide effective forensic accounting services.

Technology also helps forensic accountants to communicate their findings and recommendations to stakeholders. Forensic accountants utilize data analysis to examine large sets of structured and unstructured data. Forensic accountants use techniques like ratio analysis, vertical and horizontal analysis, and Benford’s Law to identify irregularities in financial statements.

Industry Standards and Benchmarks

Forensic accountants must follow industry standards and benchmarks, including those set by the American Institute of Certified Public Accountants (AICPA) and the Association of Certified Fraud Examiners (ACFE). They must also stay up to date on regulatory compliance, including the Sarbanes-Oxley Act and the Dodd-Frank Act.

Industry benchmarks and standards help forensic accountants to provide high-quality services and to identify potential areas of financial fraud. Forensic accountants must be able to work with accounting professionals, law enforcement agencies, and government agencies to investigate financial crimes.

Collecting and Analyzing Data

Forensic accountants must collect and analyze relevant data to identify financial anomalies and potential areas of financial fraud. They use financial statements, financial reports, and other data sources to evaluate a company’s financial health and performance. They perform in-depth reviews of books and records to investigate potential fraud or financial misconduct.

Thus, forensic accountants must have strong analytical skills and the ability to identify trends and patterns in financial data. They must also be able to communicate their findings and recommendations to stakeholders.

Performing Ratio Analysis

Ratio analysis is a critical component of forensic accounting, including the evaluation of a company’s profitability, efficiency, and leverage. Forensic accountants use financial ratios, such as the current ratio and the debt-to-equity ratio, to assess a company’s financial health.

Leverage ratios, such as debt-to-equity and interest coverage, are used to evaluate a company’s debt levels, solvency, and ability to meet financial obligations by analyzing data from the balance sheet and income statement.

Liquidity ratios assess a company’s ability to pay off its short-term liabilities. Solvency ratios evaluate a company’s ability to meet its long-term obligations.

They must have a strong understanding of financial analysis techniques, including trend analysis and horizontal analysis. Forensic accountants use ratio analysis to identify potential financial anomalies and areas of financial fraud.

Financial ratios help assess a company’s profitability, liquidity, and solvency over time. Key solvency ratios include debt-to-equity and interest coverage ratios. The current liability coverage ratio assesses a company’s ability to cover its current liabilities with the cash flow from its operations.

Analyzing Trends Over Time

Trend analysis is a critical component of forensic accounting, including the evaluation of a company’s financial performance over time. Forensic accountants use trend analysis to identify patterns and anomalies in financial data. They must have a strong understanding of financial analysis techniques, including horizontal analysis and ratio analysis.

Forensic accountants use trend analysis to identify potential areas of financial fraud and to evaluate a company’s financial health. Analyzing trends over time helps stakeholders identify patterns that indicate future performance.

Comparing with Industry Standards

Forensic accountants must compare a company’s financial performance with industry standards and benchmarks. They use industry averages and benchmarks to evaluate a company’s financial health and performance. Leverage analysis uses ratios, such as the debt-to-equity ratio, to indicate how much a company relies on debt to finance its operations.

As mentioned, forensic accountants must have a strong understanding of financial analysis techniques, including ratio analysis and trend analysis. They must also be able to communicate their findings and recommendations to stakeholders. Comparing a company’s performance against industry standards helps understand its competitive positioning and risk profile.

Conclusion and Future Directions

Forensic accounting is a critical field that requires strong analytical skills, knowledge of financial processes, and investigative skills. They must stay up to date with industry benchmarks, regulatory compliance, and new technologies. The field of forensic accounting is constantly evolving, with new challenges and opportunities emerging regularly. Consequently, forensic accountants must adapt to these changes and provide high-quality services to their clients.

ABOUT GARY RUSHIN

Gary Rushin is a CPA, former investment and commercial banker, and turnaround executive with decades of experience helping founders, boards, and investors uncover the real story behind the numbers. His career began on Wall Street analyzing S&P-rated companies, where he developed the accounting rigor and investigative mindset that now define his forensic approach to financial analysis.

Over the years, Gary has served as a CEO and CFO, guiding distressed companies through complex restructurings, uncovering hidden risks, and rebuilding financial systems capable of supporting long-term growth. He has worked across industries—from technology and manufacturing to corporate services—leading teams through high-stakes transitions where accurate financial reporting, internal controls, and transparency determine survival.

As an educator and advisor, Gary teaches entrepreneurs, analysts, and finance leaders how to interpret financial statements through a forensic lens. His work focuses on building investor-ready companies with strong governance, credible financial disclosures, and accounting strategies aligned with economic reality—not cosmetic performance. Through his platforms, Gary Rushin Unplugged and WealthE Skool, he shares practical frameworks, case studies, and tools that help founders make smarter decisions, avoid financial blind spots, and protect the value they’ve built.

At the heart of his mission is a simple belief: numbers don’t mislead on their own—people do. And with the right training, every founder, CFO, and investor can spot the red flags before they become costly mistakes.