Learn how the 83(b) election can benefit startups and founders. Understand the implications and make informed equity decisions.

Introduction to Tax Planning

Startups must understand their tax obligations and filing deadlines to manage taxes effectively and avoid costly mistakes. Because these deadlines differ by tax type and state, founders should stay alert to local and federal filing schedules. Failing to meet deadlines can trigger penalties—federal fines often reach 5% of unpaid taxes for each month a return is late.

Understanding capital gains, federal income tax, and tax credits helps reduce overall tax liability and maximize savings.

Business Structure and Taxes

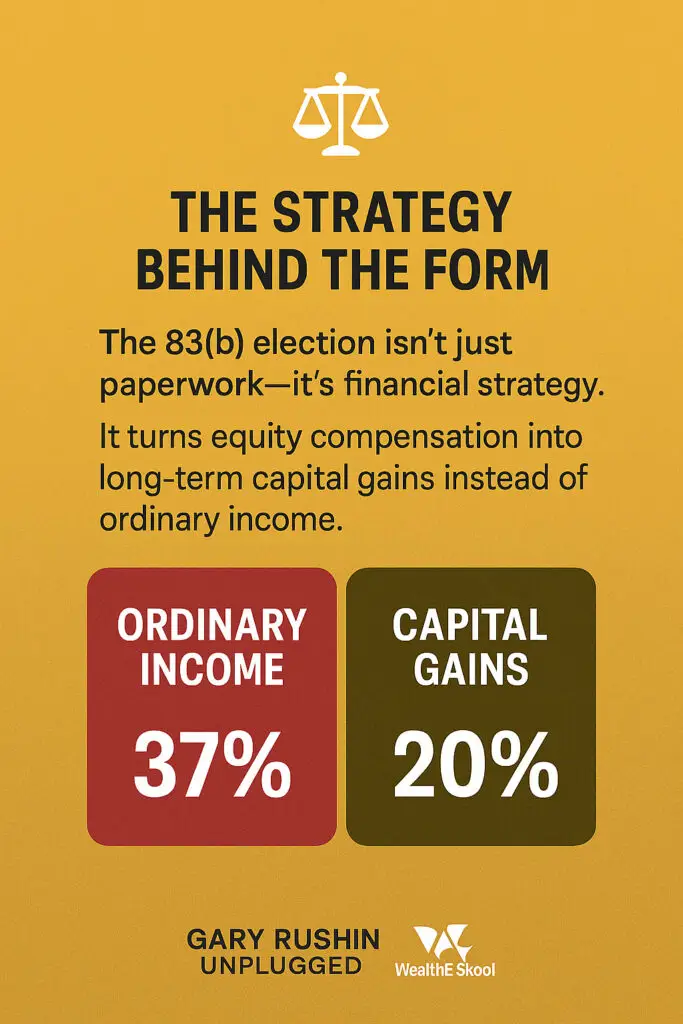

The 83(b) election is a special tax provision that lets employees and founders pay taxes on the value of their restricted stock—or early-exercised stock options—at the time they receive or purchase the shares. This is rather than waiting until the shares vest. By making this election, individuals pay taxes based on the stock’s value at the grant or exercise date, which is often much lower than its value when the shares vest.

This strategy can be a smart move for those who expect the company’s stock to rise significantly. It allows them to lock in a lower tax bill and potentially qualify for long-term capital gains on future appreciation. Without the 83(b) election, employees must pay taxes when their stock vests, which may result in a higher tax bill if the stock’s value has increased. However, early exercising stock options can create liquidity challenges since private shares are difficult to sell.

Taxpayers must file the 83(b) election within 30 days of exercising their options to pay taxes at the time of exercise rather than vesting. For anyone receiving restricted stock or early-exercised stock options, understanding the 83(b) election is critical for effective tax planning. This includes minimizing future tax liabilities.

Equity Compensation

Startups often offer equity compensation, including stock options and restricted stock, to employees and founders, which can provide tax benefits.

Restricted stock units (RSUs) typically convert into common stock upon vesting, giving employees voting rights and potential dividends.

Understanding the differences between incentive stock options and non-qualified stock options is essential for tax planning purposes. Both incentive stock options (ISOs) and non-qualified stock options (NSOs) are taxed on the spread between the strike price and the fair market value at exercise. Exercising stock options early can trigger minimal or no taxes when the spread is small. Exercising stock options early means that if employees leave the company before vesting, the company may buy back unvested shares. Equity compensation can also align employees’ interests with the company’s success.

Ordinary income tax and capital gains tax must be considered when issuing or exercising stock options.

Types of Equity Compensation

Certain types of equity compensation provide immediate value through tax credits or other financial incentives. Startups qualify for the R&D tax credit when they invest in innovation and research to develop new products or processes. To qualify, a startup must have gross receipts below $5,000,000. Many unprofitable startups save money on payroll taxes by using R&D tax credits.

R&D tax credits help unprofitable startups reduce their payroll tax burden. The credit lowers a startup’s tax bill and can even lead to capital gains if its innovation succeeds. Eligible startups can use R&D tax credits to offset up to $500,000 in expenses beginning in the 2023 tax year. Startups can save as much as $250,000 annually in payroll taxes through R&D credits, and the IRS plans to double this limit to $500,000 starting in 2023.

Stock Options and Tax Reporting

- Taxpayers must report stock options to the Internal Revenue Service and follow all tax laws and regulations to avoid penalties. They must also comply with specific sections of the Internal Revenue Code when reporting stock options.

- Taxpayers must file tax forms, such as Form 3921, to report stock option exercises and other equity compensation events. Tax forms and reporting requirements may change from year to year, so staying updated is essential.

- Startups must comply with both federal and state tax laws, including tax filing and payment obligations. Startups with employees should monitor quarterly and annual payroll tax filings. Every startup that holds an Employer Identification Number (EIN) must file annual tax returns, even if it shows no profit.

- The IRS taxes stock options when employees exercise or vest them, depending on the type of option.

Incentive Stock Options

Incentive stock options can offer tax benefits to employees. Deferred taxation and potential long-term capital gains treatment, which may result in a capital gain when the stock is sold after meeting the holding requirements, are included.

However, incentive stock options are subject to alternative minimum tax and other tax rules and regulations. Exercising incentive stock options can increase an employee’s taxable income, potentially triggering alternative minimum tax. Exercising early could result in an alternative minimum tax (AMT) for ISOs or ordinary income tax for NSOs. This depends on the exercise circumstances.

If a company fails, employees cannot recoup their investment by exercising their stock options early, as those shares typically lose value. To qualify for long-term capital gains tax rates on ISOs, shares must be held for at least two years after the option grant date and for at least one year after the exercise date.

Startups must carefully consider the tax implications of issuing incentive stock options to employees.

State Taxes

State taxes, including state income tax and franchise tax, must be considered when starting or operating a business.

Delaware franchise tax and state franchise tax, for example, are annual taxes imposed on corporations incorporated in Delaware. Even if a startup is not generating business income, it must still pay the Delaware franchise tax if incorporated in the state.

Franchise taxes can vary by state and may include additional taxes beyond income and payroll taxes. California imposes a corporate income tax and a minimum franchise tax of $800 for businesses operating within its borders. California franchise tax is typically due on April 15 if the startup has employees or generates revenue in California.

Startups must comply with state tax laws and regulations, including tax filing and tax payment requirements. If a startup is incorporated in Delaware, it must pay an annual Delaware franchise tax, which is due by March 1.

Startups should also be aware of other taxes and additional taxes that may apply depending on their business activities and location.

Tax Forms and Compliance

Taxpayers must file forms such as Form 1040 and Form 1120 to report income and pay taxes. Failing to submit required forms on time can trigger penalties if taxes are owed. Taxpayers must submit the federal corporate income tax return (Form 1120) by April 15 each year. Startups must also file this return annually, even if they are not yet generating a profit.

Startups must comply with both federal and state tax laws, including filing and payment requirements based on the company’s fiscal year. The due dates for estimated quarterly payroll tax filings often align with state corporate tax deadlines. Delaware imposes a $200 penalty plus interest for late franchise tax payments. Federal penalties for late corporate income tax filings can reach 25% of the unpaid tax after several months.

Strong tax compliance helps businesses avoid penalties, maintain good standing, and ensure long-term success. Maintaining accurate financial records is equally critical for both tax compliance and audit readiness.

Vesting Schedule

A vesting schedule is a critical component of equity compensation, as it determines when employees can exercise stock options or receive restricted stock. The vesting date is the specific point when restricted stock or RSUs become transferable and are recognized for tax purposes.

The vesting schedule must be carefully considered to ensure that it aligns with the company’s goals and objectives. Employees may be required to pay income taxes on the value of their equity at the vesting date, and this amount is typically withheld from employees’ paychecks.

Startups must also consider the tax implications of vesting schedules, including the potential impact on tax liability. The vesting date is critical for tax purposes, as it determines when employees must pay tax on their equity compensation.

The 83(b) Election Risks and Downside

The 83(b) Downside

The 83(b) election can be a powerful tool for reducing your future tax bill on equity compensation. Startup founders and employees must understand its potential risks before making this decision.

One of the biggest drawbacks is that you must pay ordinary income tax on the value of your restricted or early-exercised stock options at the time of grant or purchase—even if you haven’t yet earned the shares through vesting and may never do so. If you leave the company before your equity fully vests, or if the company fails, you could end up paying taxes on stock that provides no financial benefit.

Another major risk is liquidity. Because private company shares rarely sell easily, you may owe taxes on your equity but be unable to sell shares to cover the bill. This creates cash flow pressure, especially for early-stage startups where the company’s value remains uncertain.

The IRS treats the 83(b) election as irrevocable. Once you file, you can’t reverse your decision, even if your situation changes or the company’s value declines. If the stock’s value drops after you pay taxes, the IRS won’t refund your taxes, and you might not be able to deduct the loss against other income.

Strict Tax Compliance Requirement

Additionally, taxpayers must maintain strict tax compliance. The IRS requires taxpayers to file the 83(b) election form within 30 days of receiving or purchasing stock. Missing this deadline eliminates your opportunity to make the election, which could result in a higher tax bill if the stock’s value increases.

Given these risks, consult a qualified tax professional before making an 83(b) election. Careful tax planning and an honest assessment of your company’s prospects can help you avoid unexpected tax obligations and ensure that your equity compensation provides the financial rewards you expect.

Small Business Considerations

The 83(b) election can be a powerful way to reduce your future tax bill on equity compensation, but founders and employees must weigh the risks carefully.

One major drawback is that you must pay ordinary income tax on the value of your restricted or early-exercised stock at the time of grant or purchase—even if you haven’t yet earned the shares through vesting and might never earn them. If you leave the company before your equity vests, or if the company fails, you might pay taxes on stock that never delivers any financial value.

Another serious risk involves liquidity. Since investors cannot easily sell private company shares, you may owe taxes on equity compensation without the ability to sell shares to cover your bill. This creates cash-flow pressure, especially for early-stage startups with uncertain valuations.

The IRS treats the 83(b) election as irrevocable. Once you file, you cannot reverse the decision, even if your circumstances change or the company’s value declines. If the stock’s value falls after you pay taxes, the IRS won’t refund those payments, and you might not deduct the loss against other income.

Tax Planning Strategies

Tax planning strategies—such as deferred taxation and income shifting—help minimize tax liability and maximize potential savings. Maximizing deductions, like those for research and development (R&D) expenses, can substantially reduce a startup’s tax bill. Tax credits lower the actual tax owed dollar for dollar, while deductions decrease the amount of income subject to tax.

Startups must carefully evaluate the tax implications of each business decision, including the choice of legal structure and the issuance of equity compensation. Pre-revenue and unprofitable startups commonly file for R&D tax credits to reduce their tax burden. The timing of when founders or employees purchase shares also affects their tax strategies. In addition, startups should explore all available tax credits—particularly the R&D tax credit—to further limit their liability.

Strong tax planning ensures long-term business success while minimizing penalties and fines. Pass-through entities, in particular, offer unique tax advantages and planning opportunities for founders and startups.

Conclusion

Understanding the 83 b election and other tax planning strategies is essential for startups and founders to minimize tax liability and ensure long-term success.

Tax planning must be carefully considered in the context of business decisions, including the choice of business structure and the issuance of equity compensation.

By following tax laws and regulations and utilizing tax planning strategies, startups can effectively minimize their tax bill and achieve their business objectives.

ABOUT GARY RUSHIN

Gary Rushin is a seasoned CPA, former investment banker, and turnaround professional with over 30 years of experience in accounting, finance, and business strategy. He has advised Fortune 500 companies, growth-stage startups, and distressed businesses on financial restructuring, corporate governance, and risk management. Known for his expertise in forensic accounting and financial statement analysis, Gary combines deep technical knowledge with AI-driven tools to help entrepreneurs, investors, and executives uncover hidden risks, protect capital, and drive value.